In Mel Brooks’ seminal 1977 Hitchcock parody “High Anxiety”, much of the action revolves around the Psycho-Neurotic Institute for the Very, Very Nervous. Investors may feel the need to book into a similar establishment in 2019. Too many huge decisions need to be called correctly to feel relaxed about the year ahead.

Ninety years after the Wall Street Crash, global geopolitics and markets are like the person scaling a building on our front cover — in an exposed and precarious position.

And it’s a long way down. That’s why Reuters Breakingviews’ Predictions 2019 book is also titled “High Anxiety”.

Most investors already understand that Federal Reserve Chairman Jerome Powell and his fellow central bankers could get it wrong on rates, and exacerbate an outlook in which major economies are likely to expand more slowly. What may be less obvious is which companies will roll with the punches, and which will finish 2019 laid out on the canvas.

Private equity, where deals are being done at high prices with lots of debt, is the perfect starting point. Our view is that the real fall guys from lower returns won’t be storied buyout barons like Blackstone, but those who have advanced them credit on generous terms. An exception is Masayoshi Son, whose $97 billion Vision Fund will have some difficult conversations with its investors as it writes down a spate of overpriced purchases.

This could be happening at the same time as geopolitical strains draw parallels with another classic film, “High Noon”. A December détente between U.S. President Donald Trump and his Chinese counterpart Xi Jinping is a step forward, but relations between the two largest economies remain tense, and could worsen. In the corporate corral, guns will be drawn between activist investors and the French establishment, where we predict Vivendi and others are vulnerable.

Britain’s attempts to leave the European Union could yet avoid disaster, but a GDP-sapping no-deal in March is still a major risk. Italy will continue to rile the European Union, which could branch off in a more eurosceptic direction with European Parliament elections in May. Italian banks will bear the brunt of any return of “Quitaly” risk.

And the potential for the U.S. Congress to do what Trump won’t — sanction Saudi Crown Prince Mohammed bin Salman for the murder of journalist Jamal Khashoggi in October by Saudi agents — could destabilize the Middle East. But Trump now has the leverage to push MbS to undo many of his blunders — and keep oil prices low — and would be foolish not to use it.

For some, 2019 will be a year of recovery, and even success. Long-suffering Deutsche Bank has the scope to surf a wave of higher fixed-income trading revenue if rates keep rising. Italy’s woes could give Moncler boss Remo Ruffini a chance to remake his firm into an Italian version of Bernard Arnault’s LVMH. Rio Tinto will finally turn big miners into big spenders, Facebook could turn out to be the JPMorgan of tech, and Airbnb will succeed where others failed in China.

Meanwhile, businesses will continue to wrestle with the need to embraceenvironmental, social and governance issues — one area to watch is how actively banks use their bully pulpits to lobby gun manufacturers. With its traditional U.S. relationship in flux, look out for Saudi oil to be priced in yuan, boosting Beijing’s attempts to create a non-dollar hegemony. And a quarter-century after genocide, Rwanda will show the world that a single market with Ethiopia is better for growth than trade barriers.

What gives us the confidence to make these calls in an era when experts are shouted down? One reason is that they often turn out to be correct — witness last year’s forecast on bitcoin’s big wipeout. The cryptocurrency dropped from over $18,000 to under $4,000 during 2018. True, only half a side of SLAW was delivered with the IPO of Spotify and filing by Lyft to go public — but we’ll watch for Airbnb and WeWork to complete the acronym in 2019. And we said Amazon would bid for EU soccer, but didn’t expect football rights to fall in value.

Our overriding motivation is to provide thought-provoking, research-basedpredictions that don’t follow the herd. In 2019, investors can only hope that Powell and his central bank peers are similarly independent-minded.

George Hay

Associate Editor, Reuters Breakingviews

January 2019

…

CONTENTS

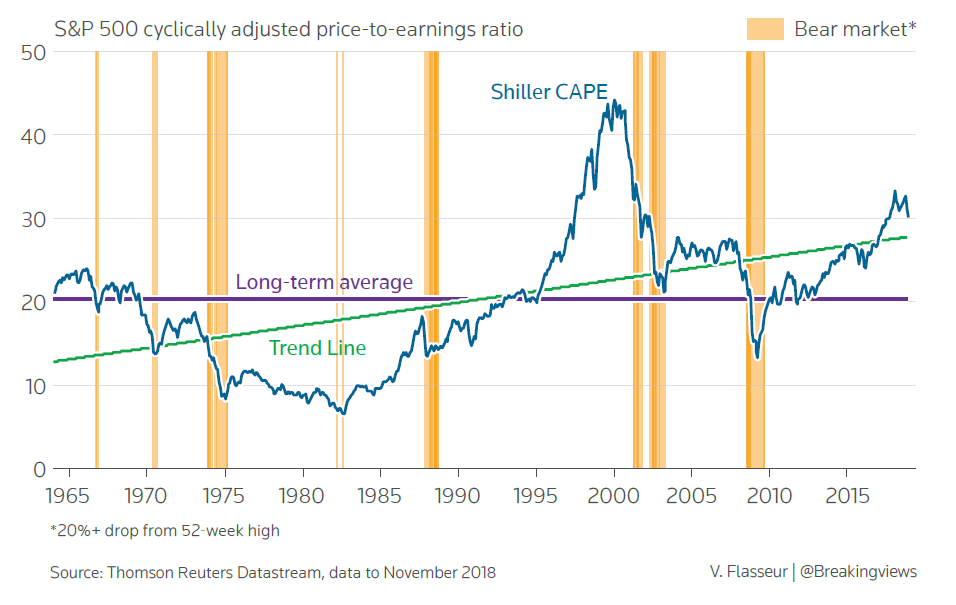

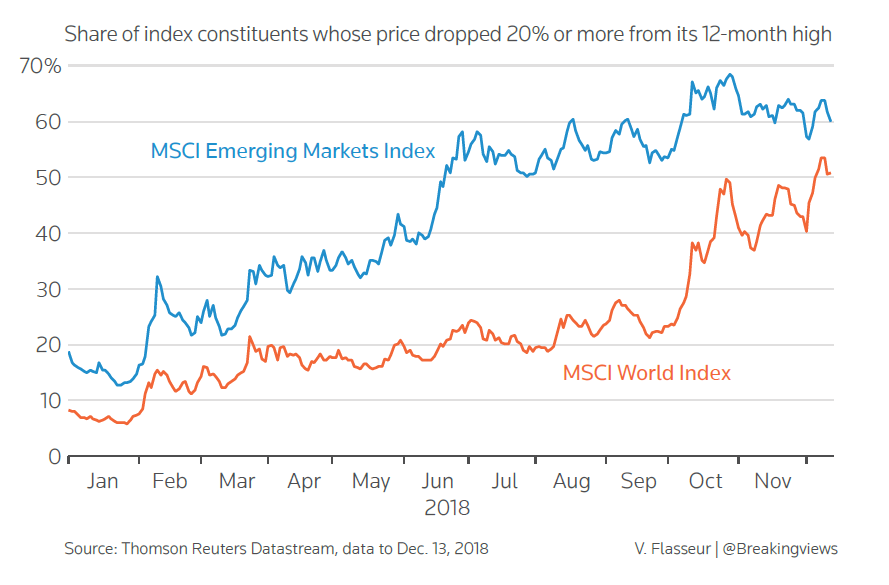

Global equities offer value trap in 2019

China-U.S. trade war will get a lot more personal

Private equity returns will drop a digit

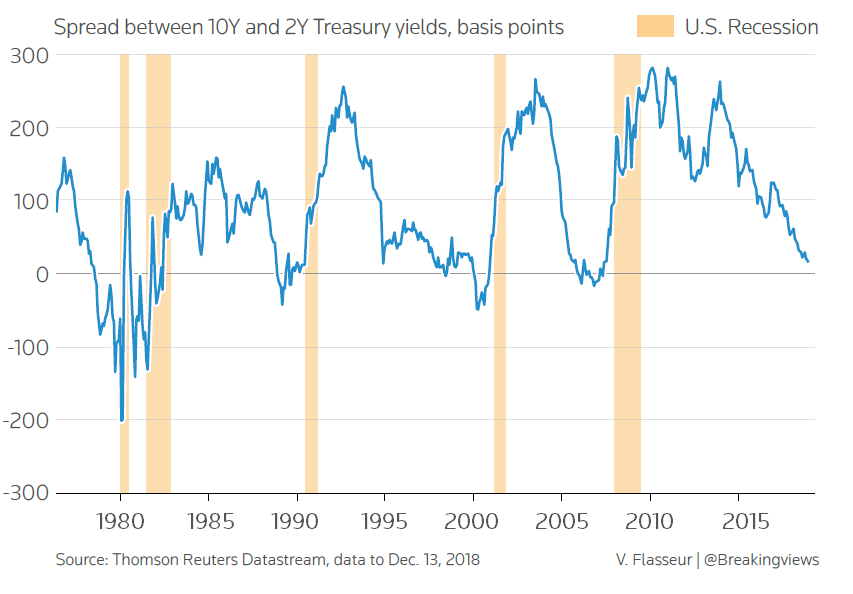

Three key indicators to watch like a hawk in 2019

Tech to disrupt supply chains more than trade wars

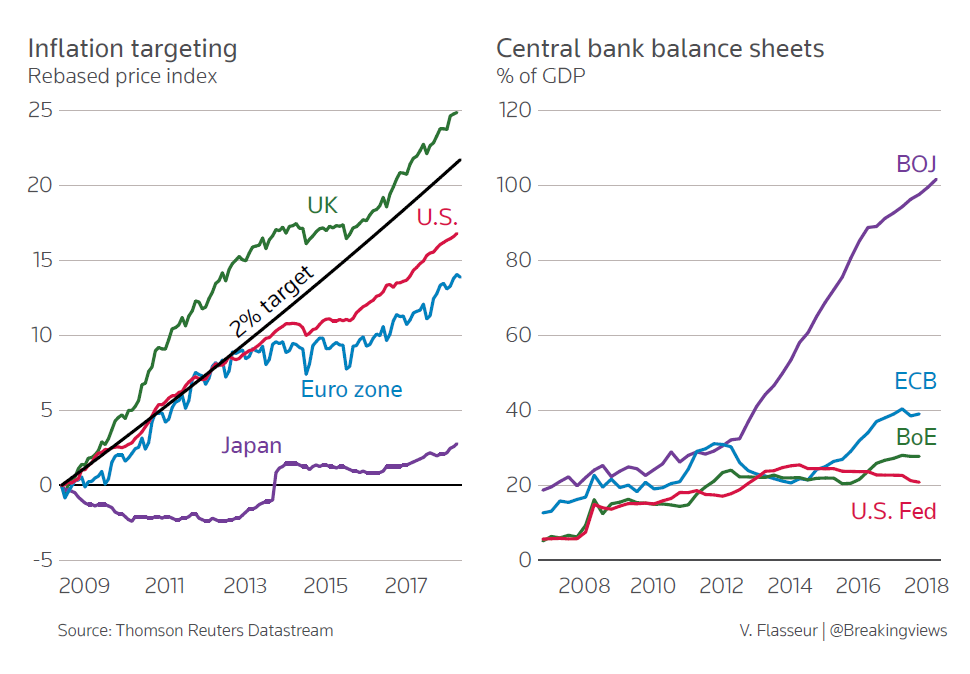

Japan is stealth threat to 2019 market stability

SoftBank writedown will cloud Son’s way forward

Activism anxiety will grip French establishment

Facebook might be the JPMorgan of the tech world

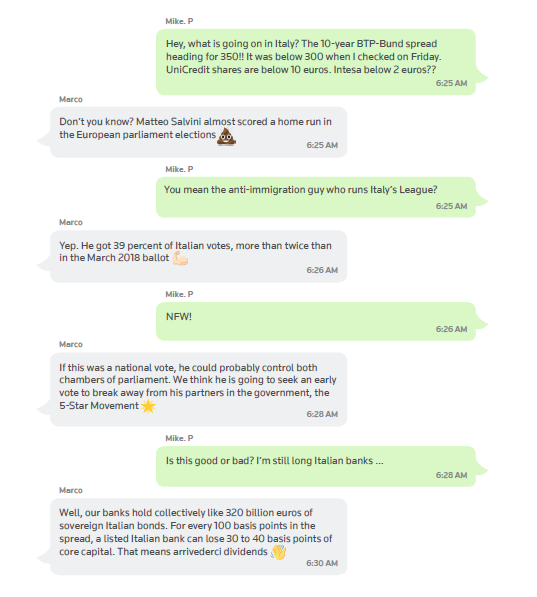

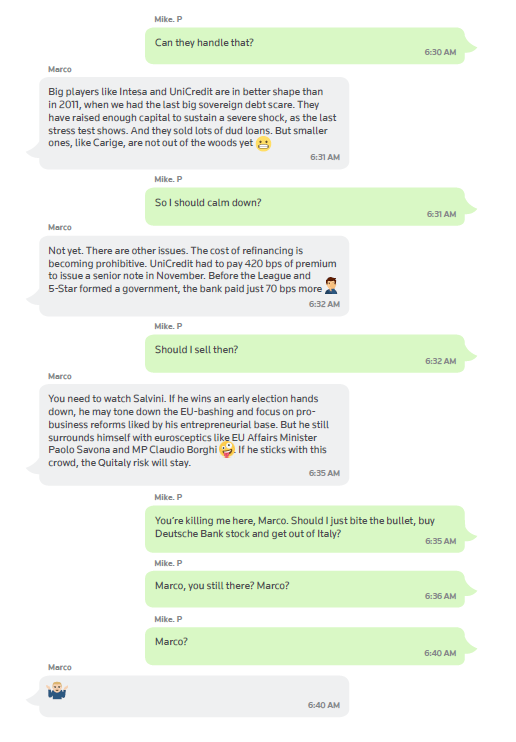

Italian banks to bear populism’s burden next year

Trump can get what he wants from Saudi in 2019

Memo to Theresa May: How to save Brexit as well

Goldman Sachs will spend 2019 in velvet handcuffs

Buyout lenders will enter a new world of pain

A made-in-America market will be a distorted one

General Electric can go from bad to worse in 2019

Brazil will get energy mostly right; Mexico won’t

Lyft, Uber IPOs will drain Tesla’s scarcity value

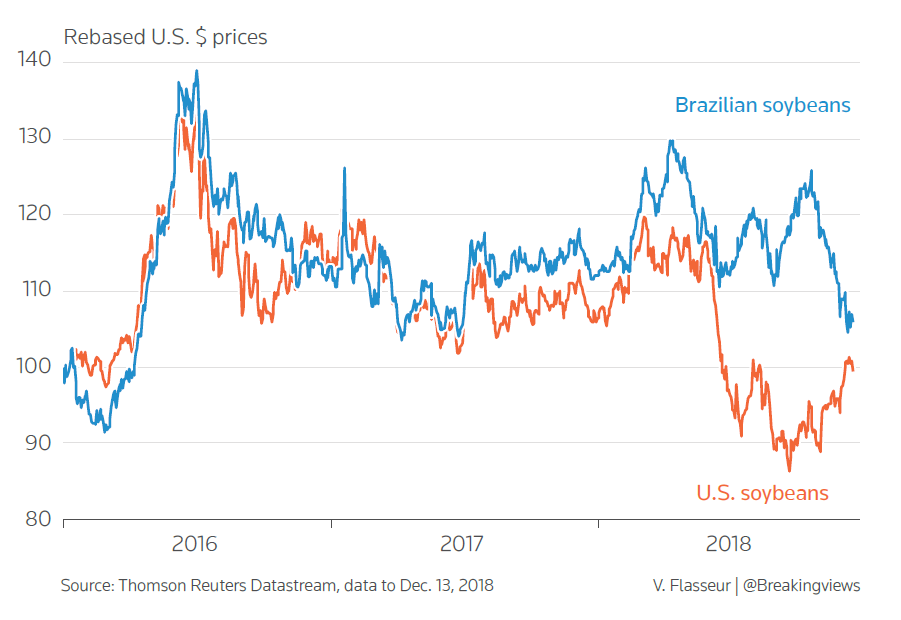

Financing drought cracks farmers’ loyalty to Trump

ByteDance will take over B in China’s BAT

Airbnb will succeed where U.S. peers failed: China

Deutsche Bank will be unlikely 2019 trading star

Italy’s woes could spell LVMH moment for Moncler

East Africa will buck global great rift trend

Rio will turn big miners back into big spenders

Starbucks will start brewing a venti Chinese deal

Chinese startups will get thrown an M&A lifeline

Saudi oil will grease China’s currency ambitions

Jeff Bezos starts to resemble Sam Walton

Keep an eye on Seoul for Asia’s next big buyer

Firearms will test the mettle of woke financiers

Indian unicorns will feast on richer pastures

Glasenberg successor will run a different Glencore

Next ECB boss will matter less than his sidekick

The 2019 stock market reversal: how it happened

A Trump versus Xi wrestling match might just help

Why I’m relocating to Paris in the year ahead

A century on, bet on a new Black Sox-like scandal

Cannabis will take China tech’s path to propriety

World will improve where it matters most in 2019