BY CHRISTOPHER THOMPSON

Whisper it gently: Deutsche Bank shareholders might finally have something to cheer about. The German lender has in recent years seen seemingly irreversible declines in trading revenue that have outpaced cost-cuts. In 2019 its business mix, and the potential for currency volatility and rising European rates, should make it a relative winner.

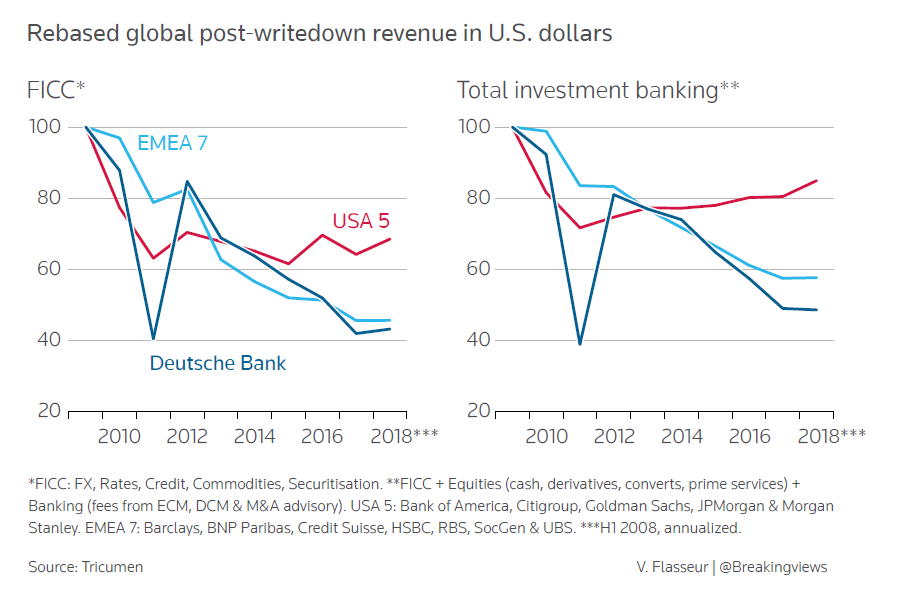

Ever since the financial crisis Europe’s investment banks have resembled a car crash in slow motion. The region’s lenders have seen their overall investment banking revenue decline by 27 percent since 2010, according to UBS, compared to an 18 percent decline globally. Deutsche has been even worse — at its bedrock fixed-income trading division, which in 2017 accounted for 17 percent of group net revenue, turnover has dropped by 28 percent over the last two financial years alone. Its shares trade at a pitiful, Greek bank-style valuation of just 0.3 times tangible book. Deutsche Bank executives have had to repeatedly deny reports that a defensive merger with Commerzbank is in the offing.

Fixed-income traders tend to thrive when there is a trend. The last time this occurred in Europe was when European Central Bank President Mario Draghi introduced quantitative easing in 2015 and guided steadily lower interest rates. Consequently, asset managers increased buying and selling and companies purchased more hedging products. As the ECB prepares to scale down its asset purchases, the next trend is rising yields. Given that Deutsche has the biggest market share in European rates apart from JPMorgan , its top line should benefit disproportionately from heightened client demand.

Political volatility could add some additional gloss in currencies. Continued geopolitical uncertainty in Europe — think Brexit and Italy — and elsewhere should lead to wider currency spreads and, all else being equal, greater profits.

Chief Executive Christian Sewing has zero room for complacency. A boost in European trading income will be somewhat offset by falling U.S. revenue due to cutbacks in Deutsche’s U.S. rates and equities business. At the same time, Sewing must find another billion euros in cost savings, and firefight Deutsche getting dragged into questions over money-laundering controls.

Analysts only forecast a 3 percent return on tangible equity for Deutsche in 2019. But the bank’s increasingly diverse shareholder register — which encompasses Qatari, Chinese and U.S. hedge fund investors — doesn’t need rising European rates to lead to a miraculous resurgence. Just a transition from terrible to merely bad.

First published Dec. 27, 2018.